Thinking about the knock-on effects of the Great Pandemic of 2020 is enough to make anyone philosophical – and Stewart Butterfield more than most.

In the three months since companies worldwide switched off the lights and sent their employees home, it has become more obvious by the day that millions of workers are now permanently unbound from their cubicles. “There are second- and third-order effects to this,” Mr. Butterfield says via Zoom from his house in San Francisco, his hair dishevelled and face bestubbled (although not necessarily any more than was the case before the pandemic). “What does it do to the commercial real estate market, to the tax base and to the restaurants next to office buildings? What does it do to the distribution of high-income jobs around the country?” Do people in Toronto making $150,000, he wonders, continue making the same salary even if they decide to move back to Manitoba to be close to their elderly parents? And what does that do to the economies of smaller towns, where houses cost $80,000 instead of $800,000? “There are so many things you can’t really even imagine the net effect of,” he says.

Granted, Mr. Butterfield is prone to deep thinking, what with his master’s degree in philosophy from Cambridge. But he’s also the Canadian co-founder and chief executive of Slack, the company that has, in large part, enabled the dissolution of decades of office culture – a generational shift with massive cultural and societal implications.

When an oil market war broke out between Russia and Saudi Arabia on March 8, it triggered the worst single-day price collapse since the early 1990s. As petroleum-producing nations, including Canada, have grappled with the fallout the price plunge has drawn comparisons to the oil routs that occurred in 2008, during the Great Financial Crisis, and in 2014 when markets finally caught up with America’s shale boom.

It’s tempting to view all three downturns as separate episodes, but everything that’s happened since 2008 has been the back end of a boom that more or less began in 1998. That was when oil prices finally bottomed out after crashing in 1980 and begun their epic climb.

I created the following chart a few years ago for a story for Maclean’s, and I’ve kept updating it since. (I’ll continue to do so on this page.)

It tracks what happened after that 1980 oil bust, overlaid with the price of crude since the 2008 peak, all adjusted for inflation.

(Updated April 20)

This is by no means a forecast, but it does provide some perspective on what we’re seeing now. As painful as this latest bout of low prices is for Canada’s oil producing regions—which layers on top of the economic trauma wrought by the Covid-19 shutdown—the path oil took after the 1980s bust shows further declines in the future would not be unprecedented. If this downturn lasts as long as the rout after 1980, that would entail another seven years of slumping prices. Even if OPEC and Russia reach a truce, there is little on the horizon to suggest an impending reversal.

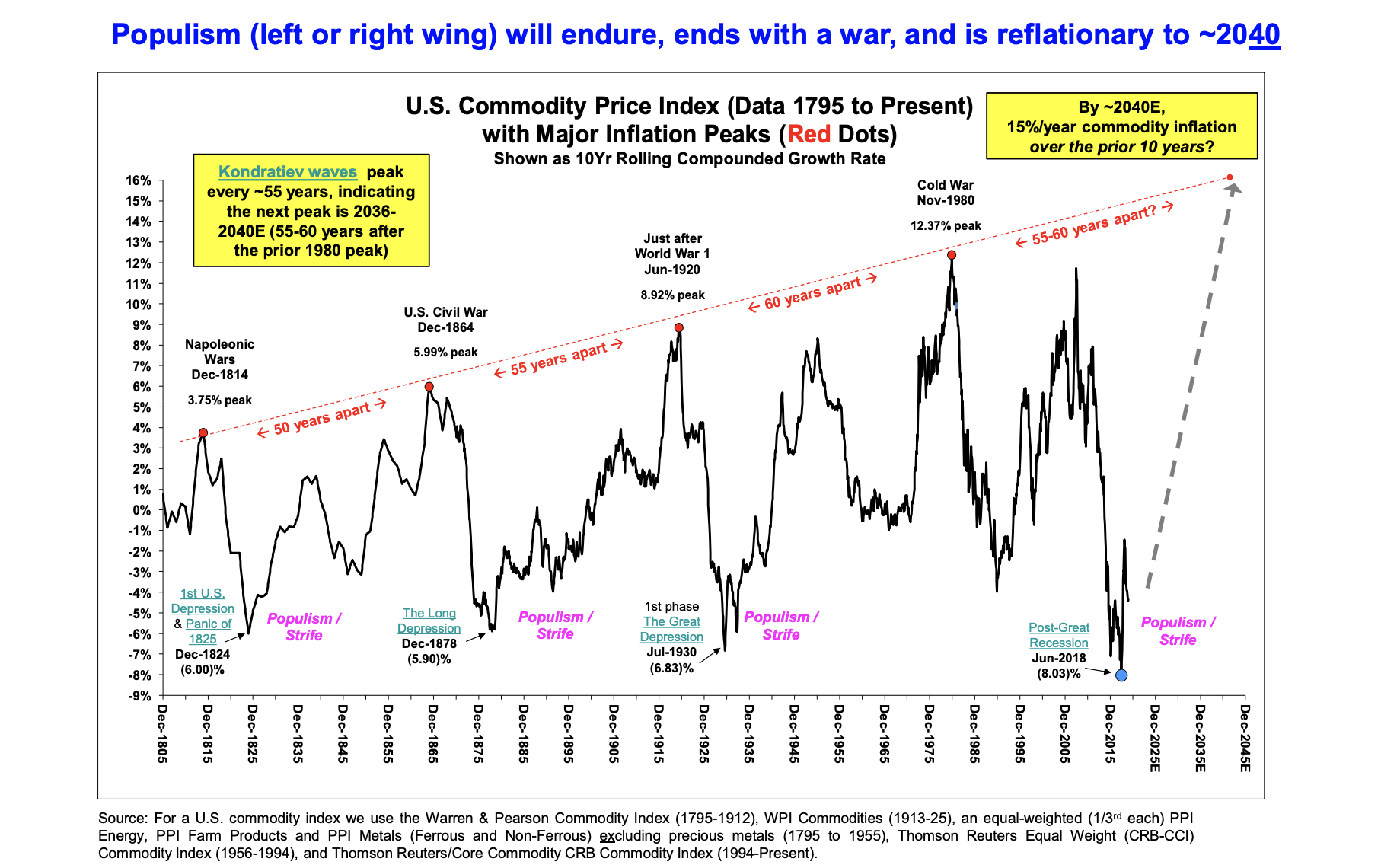

Having said that, it would also be unprecedented if the price of oil doesn’t eventually rise again. The chart below comes from a December outlook report by Stifel, a U.S. investment bank, and it tracks the long term growth rate of inflation-adjusted commodities since 1795. The boom and bust cycle that every commodity producing nation is familiar with is on display. As is the long-run cycle of populism, strife and conflict. With the emergency break pulled on the economy and a global recession of unknown depth and duration now unfolding, there’s little reason not to expect an era of domestic and international tension will follow.

Bombardier’s move to shrink itself from one of the world’s largest manufacturers of planes and trains to solely a maker of private business jets struck analysts as bold when it was announced a little over a month ago.

As panic over coronavirus threatens to flatten the aviation industry and tip the global economy into a deep funk, that decision to bet Bombardier’s entire future on a sector known for its intense turbulence looks increasingly precarious.

“[Bombardier] is in an unenviable position right now of being in an industry that’s very susceptible to a downturn,” said aviation analyst Brian Foley of New Jersey-based Brian Foley Associates. “Companies get nervous when they’re buying a private aircraft and if previous history is any indication, this could be a period of rough sledding for the industry.”

From the 1969-1970 Bombardier annual report showing the board of directors, including Laurent Beaudoin, centre.

When Bombardier launched its first Ski-Doo snowmobile in 1959, it was initially targeted at trappers, prospectors and anyone else isolated by snow and ice. But the bright-yellow machines soon became a hot toy for affluent sports enthusiasts across North America and Europe, and by the time the company went public on the Toronto Stock Exchange a decade later, Ski-Doo sales were exploding. Bombardier’s revenues in 1970 came in at nearly $1 billion, when measured in today’s dollars, up a whopping 60 per cent in just one year.

So you can forgive Bombardier’s president, Laurent Beaudoin, for his swagger in the company’s first annual report that year. Bombardier “has proved itself to be one of the most important industrial and commercial organizations in Canada,” he crowed, while the report said the snowmobile industry was “riding the crest of the leisure market [and] the wave shows no sign of cresting . . . All forecasts point to a positive and continuing upsweep of the trend well into the 21st century.”

Instead, within three years Bombardier was in serious trouble, caught out by the 1970s oil crisis and a glut of snowmobiles on the market from more than 100 rival companies, which caused its revenues to plunge.

Steve Jobs while presenting the iPad in San Francisco 27th January 2010 (Matt Buchanan, Flickr)

A decade ago I traveled to San Francisco for Canadian Business to take in the launch of Apple’s newest device at the time, the iPad. From the February 2010 issue of Canadian Business, here was my take on Steve Jobs the Magician:

It’s a mild January morning in San Francisco, and the circus has come to town. Outside the Yerba Buena Arts Center, a mob has gathered to witness the unveiling of Apple’s latest creation, a handheld computer that all the world will soon know as the iPad. Network TV crews have set up camp, their satellite dishes pointed skyward. A crush of reporters and bloggers jostle past burly security guards like kids pushing their way into a rock concert. Even after the doors close and Apple’s turtlenecked CEO, Steve Jobs, launches into what is arguably the most important presentation of his life, outside, the people keep coming.

Rafael Fischmann, a tech blogger from Brazil, travelled 18 hours just to be close to the event, “because something very big and revolutionary is coming.” Dr. Bernd Weidner, a Berlin physicist in town for a major photonics conference taking place across the street, is thrilled just to find himself in San Francisco “at this moment in history.” In fact, throughout the morning several groups of photonics experts, people who study the very building blocks of light, converge on the Apple event like moths to a torch. “This is going to be a game changer,” predicts Conor Evans, an instructor at Harvard University and an avid Apple fan.

Finally Raghavan Rajagopalan, a St. Louis — based medical researcher who’s been listening to others heap praise on Apple, cuts in. “I don’t get it,” he says simply. “There are thousands of products [at the photonics conference] to help cure cancer, amazing research into all kinds of things. But the whole world is over here watching Apple bring out some little device.”

Welcome to the $200-billion Steve Jobs magical mystery extravaganza. Jobs the Magnificent is the act everyone has come to see. It’s not always easy to articulate exactly how Jobs is able to wield such uncanny power over the consumer imagination, but the launch of the iPad provided some of the clearest examples of his unmatched, some might say mystical, powers.

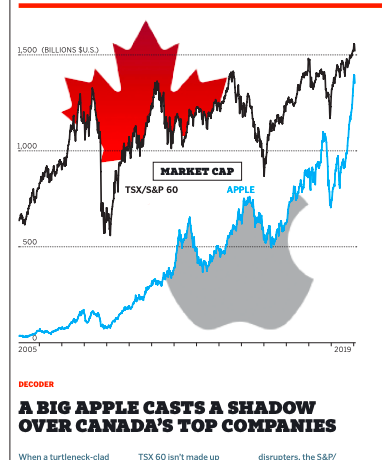

When a turtleneck-clad Steve Jobs unveiled the first iPhone in June 2007, Apple was already massive, with a market capitalization of US$100 billion. But Research In Motion, as BlackBerry was then called, was no slouch — later that year, it would rocket past Royal Bank of Canada to become the most valuable firm in this country, with a market cap of more than US$70 billion.

Thirteen years later, Apple is a $1.4-trillion juggernaut and the world’s most valuable company.

In the fall of 2009, as green shoots emerged from the ashes of America’s economy and the panic wrought by the Great Recession turned to outrage over the taxpayer bailouts handed to the very Wall Street banks whose reckless lending and disastrous bets caused the crisis, filmmaker Michael Moore debuted his latest documentary, Capitalism: A Love Story. It was anything but an ode to America’s economy. Moore’s film took angry aim at a laundry list of recent ills he blamed on an “evil” capitalist system: inequality, corrupt politicians, Wall Street’s casino-like mentality and out-of-control corporations.

As with all of Moore’s earlier documentaries, an underlying theme in Capitalism was his criticism of the way corporations concern themselves primarily with turning a buck for shareholders, damn everything, and everyone, else.

Who would have thought that almost exactly one decade later, America’s biggest capitalists would be saying the same thing?

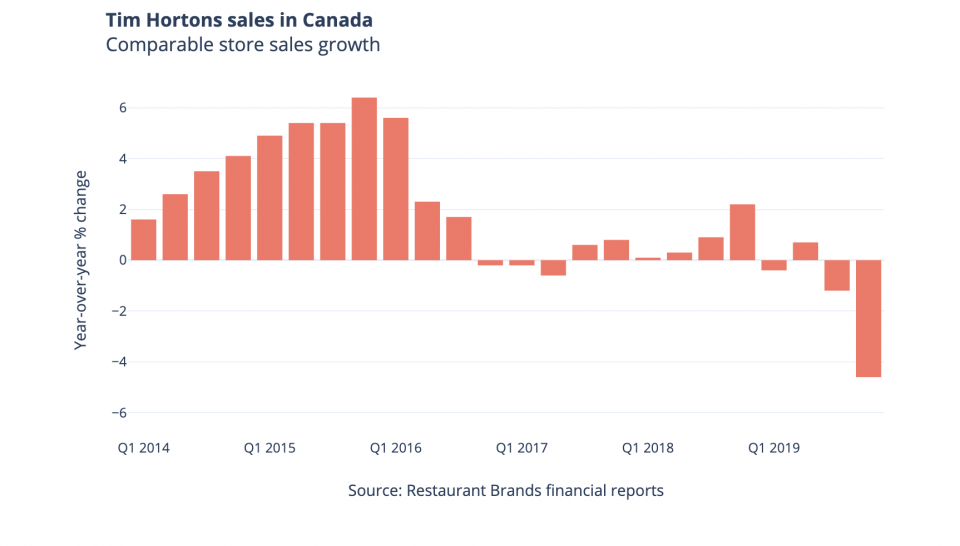

Tim Hortons has a serious Canada problem. Simply put, too many Canadians no longer think of Timmies as the folksy Canadian coffee and donut shop it once was. And they’re abandoning the chain in droves.

The latest financial results of Restaurant Brands International, the quick serve restaurant conglomerate that owns Tim Hortons, tell the bitter tale. In the fourth quarter same-store sales at Tim Hortons in Canada, a measure that tracks the performance of locations that have been open for 13 months or more, fell 4.6 per cent. The awful results in the last quarter were partly due to the large number of coffee giveaways through the Tim Hortons loyalty program, a rewards scheme the company now plans to overhaul, but this is a problem that’s been building over the past four years. Canadians have lost faith in Tim Hortons.

What auto manufacturing in Canada looked like in 1961 when it took 30 workers to produce $1 million of output. Today it takes eight. (Library Archives Canada)

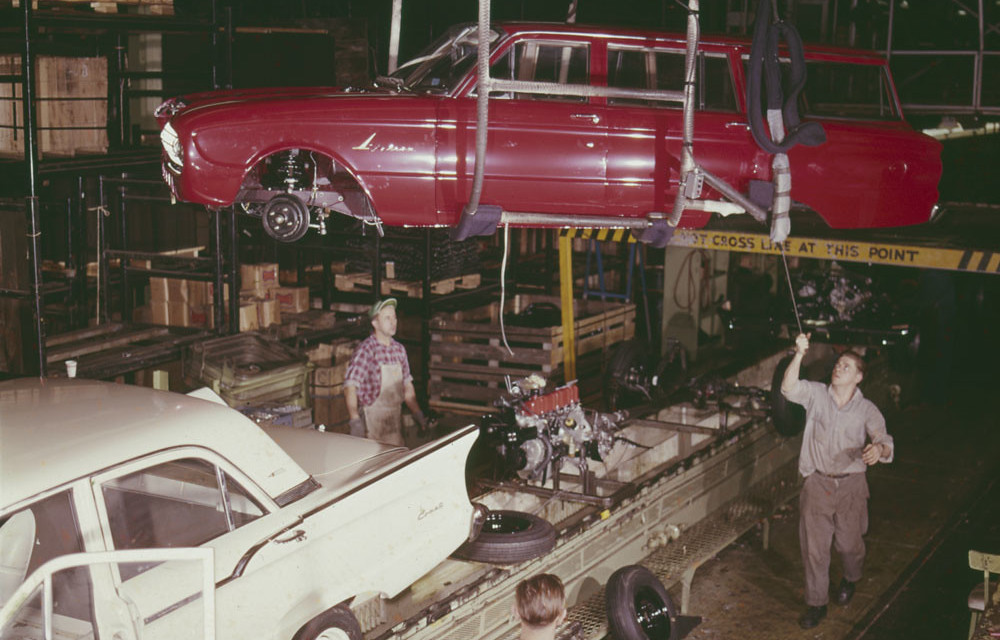

At 2 pm on Dec. 18 the last truck rolled off the line at the General Motors assembly plant in Oshawa. The closure means the loss of 2,300 jobs. A clutch of 300 workers will stay on at the plant stamping panels and doors, and the site is being converted for testing autonomous vehicles.

The demise of the assembly plant caps a long, dark decade for manufacturing in Canada. Will the 2020s be better?

Well, if the trend holds the coming year will see the industry finally recover to its pre-Great Recession high of 15 years ago. But that’s only when measured by GDP. In terms of manufacturing jobs it would be nice just to see employment recover to the level it was at before the recession in 1974.

The reality is output from factories and the number of workers in those factories have been moving in different directions for decades. That’s because technology has enabled manufacturers to do much more with fewer people.

The chart below puts that in focus. In 1961, it took 30 workers to produce $1 million of manufacturing output in Canada. Today, that same level of factory activity can be achieved with just eight workers.

The inspiration for the chart came from this 2016 Brookings piece explaining why Donald Trump’s promise to bring factories back to U.S. shores wouldn’t result in a resurgence of factory jobs, which it hasn’t.

But as the above chart shows, something is obviously missing from this post-recession period that’s exacerbated the jobs-output disconnect. Even if the long run trend in manufacturing jobs has been more or less flat for 50 years, there were still job gains during periods when output was expanding and new highs were reached. Not this time.

From 2004, when manufacturing employment peaked, to 2009 when the 2008/09 recession ended and the recovery began, factories shed 610,000 jobs, Statcan’s monthly employment data show. Since then not a single net new manufacturing job has been created for Canada as a whole. Quite the opposite — in November there were 41,000 fewer manufacturing jobs than in November 2009.

One critical ingredient has been missing over this time: private investment in things like machinery and equipment, and intellectual property products. Here’s the same chart, only now with private investment in manufacturing overlaid.

Whereas private investment once led the sector higher, over the past two decades stagnant or falling levels of investment have acted as an anchor weighing it down. As much as technology has allowed manufacturers to get by with fewer workers, underinvestment in capital, machinery and equipment is taking its toll in the form of lower productivity and that’s restraining the ability of manufacturers to expand production capacity. And so you end up with anemic growth in output and no new jobs.

Can these trends be reversed? There have been signs of a pick-up in business investment. In the third quarter capital spending rose at the fastest quarter-over-quarter pace since 2017, but it’s unclear how long that will be maintained. And while it’s true that low-cost competition from other countries means a huge number of those manufacturing jobs lost since the early 2000s are never coming back, without significant investment Canada’s manufacturing output is almost certain to remain feeble and job growth nonexistent in the decade to come.

A division of SNC-Lavalin, the engineering company at the heart of a political scandal that shook Canadian Prime Minister Justin Trudeau’s government earlier this year, has agreed to plead guilty to fraud related to its work in Libya during the last decade and pay a C$280m penalty.