Most of the world’s central banks have responded by slashing interest rates. Last week the Bank of Canada joined them with a 50 basis point cut. But while more rate cuts are expected, the ability of central banks to tackle this particularly type of crisis — supply chains have been crippled and consumers are increasingly afraid of simply going out to spend — is seen as limited. “With interest rates already so low to begin with you’re just pushing on a string with rate cuts,” says Kevin Milligan, an economics professor at the University of British Columbia. “It takes months for investment patterns to change, and that doesn’t help when something is hitting you in the short run.”

Which is why a growing chorus of economists and investors are calling on Finance Minister Bill Morneau to roll out a fiscal stimulus plan, spending heavily to shore up Canada’s economy. Morneau was already set to release the Liberals’ first re-election budget, likely at the end of March. On Monday he acknowledged Canada was in a “very volatile position” and said the federal government has the “capacity to deal with challenges exactly like this” and will introduce measures this week.

But what should those stimulus efforts look like? Maclean’s spoke with four economy watchers about what a fiscal plan for Canada’s battered economy should entail.

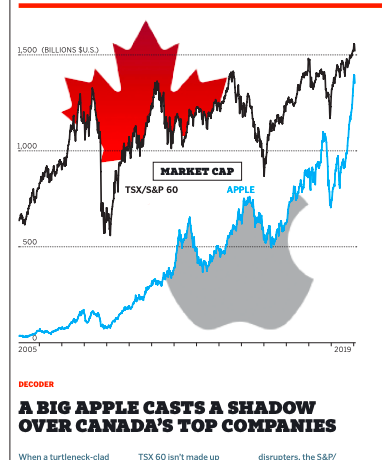

When a turtleneck-clad Steve Jobs unveiled the first iPhone in June 2007, Apple was already massive, with a market capitalization of US$100 billion. But Research In Motion, as BlackBerry was then called, was no slouch — later that year, it would rocket past Royal Bank of Canada to become the most valuable firm in this country, with a market cap of more than US$70 billion.

Thirteen years later, Apple is a $1.4-trillion juggernaut and the world’s most valuable company.

In the fall of 2009, as green shoots emerged from the ashes of America’s economy and the panic wrought by the Great Recession turned to outrage over the taxpayer bailouts handed to the very Wall Street banks whose reckless lending and disastrous bets caused the crisis, filmmaker Michael Moore debuted his latest documentary, Capitalism: A Love Story. It was anything but an ode to America’s economy. Moore’s film took angry aim at a laundry list of recent ills he blamed on an “evil” capitalist system: inequality, corrupt politicians, Wall Street’s casino-like mentality and out-of-control corporations.

As with all of Moore’s earlier documentaries, an underlying theme in Capitalism was his criticism of the way corporations concern themselves primarily with turning a buck for shareholders, damn everything, and everyone, else.

Who would have thought that almost exactly one decade later, America’s biggest capitalists would be saying the same thing?

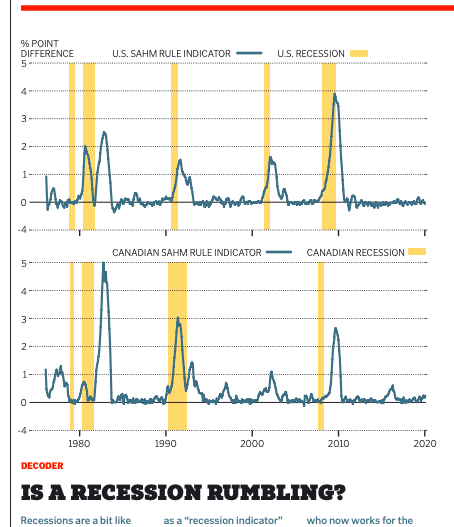

Recessions are a bit like earthquakes. They can knock you off your feet and are impossible to predict. But in the same way seismologists are working to detect quakes critical seconds before the ground starts to shake, economists are watching a new realtime gauge for signs of an imminent downturn.

It’s called the Sahm Rule, the brainchild of former Federal Reserve economist Claudia Sahm.

When Bank of Canada governor Stephen Poloz promoted Carolyn Wilkins to be his number two in 2014, he praised her as a “jack of all trades”.

Now Ms Wilkins, the bank’s senior deputy governor, has emerged as the frontrunner to replace Mr Poloz when he leaves the top job next year, in an appointment that would signal continuity while emphasising a focus on emerging challenges such as climate change and the digitisation of currency.

“If she wants the job, she will be the candidate to beat,” said Craig Wright, chief economist for Royal Bank of Canada.

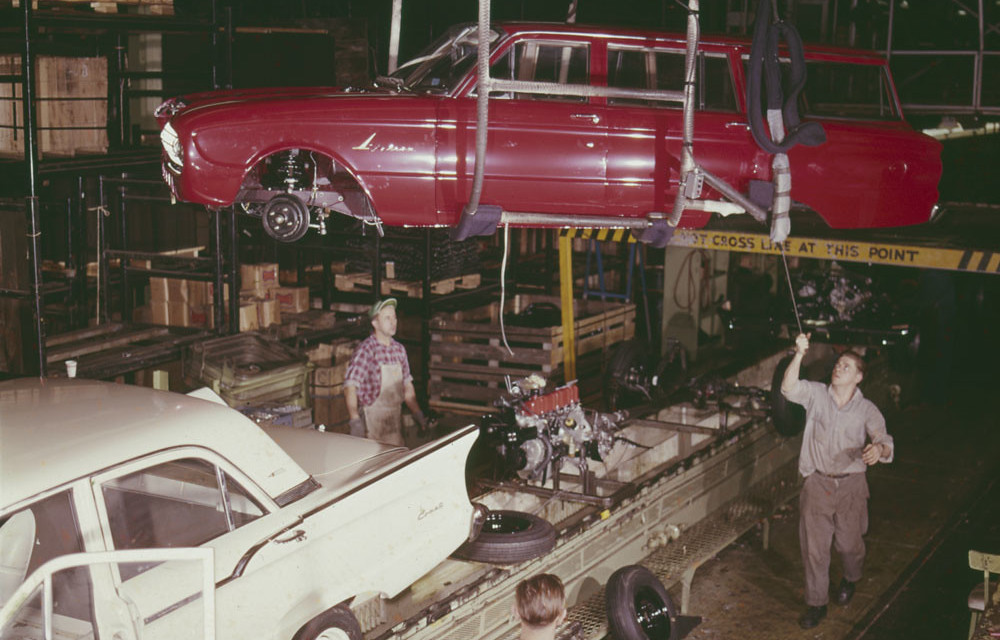

What auto manufacturing in Canada looked like in 1961 when it took 30 workers to produce $1 million of output. Today it takes eight. (Library Archives Canada)

At 2 pm on Dec. 18 the last truck rolled off the line at the General Motors assembly plant in Oshawa. The closure means the loss of 2,300 jobs. A clutch of 300 workers will stay on at the plant stamping panels and doors, and the site is being converted for testing autonomous vehicles.

The demise of the assembly plant caps a long, dark decade for manufacturing in Canada. Will the 2020s be better?

Well, if the trend holds the coming year will see the industry finally recover to its pre-Great Recession high of 15 years ago. But that’s only when measured by GDP. In terms of manufacturing jobs it would be nice just to see employment recover to the level it was at before the recession in 1974.

The reality is output from factories and the number of workers in those factories have been moving in different directions for decades. That’s because technology has enabled manufacturers to do much more with fewer people.

The chart below puts that in focus. In 1961, it took 30 workers to produce $1 million of manufacturing output in Canada. Today, that same level of factory activity can be achieved with just eight workers.

The inspiration for the chart came from this 2016 Brookings piece explaining why Donald Trump’s promise to bring factories back to U.S. shores wouldn’t result in a resurgence of factory jobs, which it hasn’t.

But as the above chart shows, something is obviously missing from this post-recession period that’s exacerbated the jobs-output disconnect. Even if the long run trend in manufacturing jobs has been more or less flat for 50 years, there were still job gains during periods when output was expanding and new highs were reached. Not this time.

From 2004, when manufacturing employment peaked, to 2009 when the 2008/09 recession ended and the recovery began, factories shed 610,000 jobs, Statcan’s monthly employment data show. Since then not a single net new manufacturing job has been created for Canada as a whole. Quite the opposite — in November there were 41,000 fewer manufacturing jobs than in November 2009.

One critical ingredient has been missing over this time: private investment in things like machinery and equipment, and intellectual property products. Here’s the same chart, only now with private investment in manufacturing overlaid.

Whereas private investment once led the sector higher, over the past two decades stagnant or falling levels of investment have acted as an anchor weighing it down. As much as technology has allowed manufacturers to get by with fewer workers, underinvestment in capital, machinery and equipment is taking its toll in the form of lower productivity and that’s restraining the ability of manufacturers to expand production capacity. And so you end up with anemic growth in output and no new jobs.

Can these trends be reversed? There have been signs of a pick-up in business investment. In the third quarter capital spending rose at the fastest quarter-over-quarter pace since 2017, but it’s unclear how long that will be maintained. And while it’s true that low-cost competition from other countries means a huge number of those manufacturing jobs lost since the early 2000s are never coming back, without significant investment Canada’s manufacturing output is almost certain to remain feeble and job growth nonexistent in the decade to come.

On the anniversary of the detention of two Canadians by Chinese authorities, Canada’s new foreign minister is under pressure to define the country’s relations with a more assertive Beijing.

With Chinese authorities now signalling that the cases of two Canadians held in China for the past year may move to trial on national security charges, calls are mounting for François-Philippe Champagne to take a firmer stance on Sino-Canadian relations.

He has said a new “framework” for relations is necessary following his appointment last month, but has yet to explain what that would entail — further frustrating critics who feel the Trudeau government has failed to articulate a coherent China strategy since taking power in 2015.

It’s back. For the sixth straight year Maclean’s asked economists, analysts, investors and financial observers to each select a chart about Canada’s economy they feel will be particularly important to watch in 2020 and in their own words, explain why.

As in past years, certain themes emerge in this year’s chart collection. The stability of Canada’s housing market and the dangerous levels of household debt remain an obvious concern, even if there’s less focus now on rising interest rates. Canada’s weak climate for business investment and the risk from global trade tensions are also top of mind among the experts. So too are environmental and energy issues. You’ll also find charts on how Canadians live, work and shop, how Canada’s waning competitiveness is holding the economy back, and even how a deficit of amorousness could lead to a slowdown down the road.

If it was only about hard economic numbers, Justin Trudeau’s Liberals might not have all that much to worry about in their bid for another four years in office. The most recent economic releases from Statistics Canada on jobs and GDP growth both delivered pleasant surprises to the upside, for which Team Trudeau wasted no time in taking credit. And with Canadians once again telling pollsters that the economy is at the top of their list of priorities, the Liberal’s message—that their strategy of deficit-driven intervention in the economy is working—might carry the day for them.

The problem for Trudeau is that a lot of Canadians don’t feel the economy has gotten better, or at least not for them.

Watching world events unfold from his pig farm in southwestern Ontario this past spring, Craig

Hulshof expected a strong summer for Canadian pork producers.

The Trump administration’s tariff fight with China had made it more costly for American producers to serve the booming Asian market. Meanwhile, the spread of African swine fever in China, the world’s biggest consumer of pork, forced the culling of millions of pigs, creating an opportunity for Canadian pork to fill the void.

Instead, pork and beef producers here now find themselves shut out of China altogether, the latest victims of worsening diplomatic relations between the two countries after Canada arrested Huawei executive Meng Wanzhou in December.

“We expected that when barbecue season started up that’s when we’d make our money,” Mr Hulshof said. “China has put a fork in it.”